You can choose a suitable debt relief option amongst several strategies if you’re worried about paying back your credit cards and other unsecured bills. Have a look at the professional debt relief options along with DIY strategies to bring your financial life back in order.

Debt relief options - What you can expect and when to opt for one

Check out the pros and cons of each of these debt relief options. It will help you choose your preferred one. Also know when you should opt for any of these debt relief strategies.

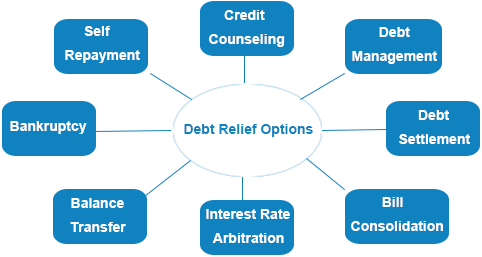

Credit Counseling

In a credit counseling session, the counselor analyzes your financial condition and offers suitable tips or suggestions following which you can repay your existing dues.

What to expect:

Pros

- Customized money management plan to manage your debts properly

- You can pay back creditors through easy repayment plans

- You can figure out whether or not you’re spending more

Cons

- May worsen your financial situation if you cannot avoid impulsive spending

When to opt for

- To manage your existing debts smartly

- You need help to plan a realistic budget

- Want to manage debts properly to improve your credit score

Debt Management

In a debt management program, the counselors of the debt relief USA companies negotiate with your creditors for a repayment plan as per your budget. You need to make a single monthly payment to the counselors, who distribute the amount amongst your creditors. This continues till you get out of debt.

What to expect:

Pros

- Reduced interest rate on debts

- A budget plan to save money

- Single monthly payment

- Possibility of less collection calls

- Positive effect on credit report and score

Cons

- Have to pay fees for professional service

When to opt for

- You’re facing problems to manage your multiple bills

- You need professional guidance

- You have a decent income to repay your debt

- You want to repay debts in full

Debt Settlement

A debt settlement program is a debt relief program which helps to reduce the outstanding balance on your bills/debts. The representative from settlement company negotiates with your creditors and/or collection agencies to reduce the payoff amount so that you can get rid of debts through a lump sum payment on each account.

What to expect:

Pros

- You can get rid of debt quickly

- Possibility of creditors/collection agencies will stop harassing you

- Become debt free through single monthly payments

Cons

- Need to pay professional fees

- Credit score may get reduced

- May have to pay tax on forgiven debt

When to opt for

- You cannot repay your debts in full

- You want to get rid of your debts fast

- You can’t negotiate with your creditors on your own

- Your financial situation doesn’t permit to repay debts in full

Bill Consolidation

When you enroll in a bill/debt consolidation program with a debt relief USA company, it analyzes your financial situation and decides upon an affordable monthly payment which you need to pay to the company. It also negotiates with your creditors to reduce the interest rates on your debts. Upon receiving payment, the consolidation company distributes it amongst your creditors as per agreement, till your dues are paid off.

What to expect:

Pros

- Single payment every month

- Interest rates may get reduced

- Complete professional guidance to pay back dues

- Credit score may get improved

- Creditors may stop troubling you for payments

Cons

- Need to pay professional fees

When to opt for

- Failed to repay outstanding dues on your own

- You can save a certain amount after meeting daily necessities

- You’re not able to manage your multiple bills properly

- Professional guidance can help you manage your financial obligations

Interest Rate Arbitration

You take out a secured loan from a lender or a financial institution at relatively low interest rate and repay your outstanding dues with the amount. Then, you repay the new loan, which is a type of debt consolidation loan, through lower monthly payments.

What to expect:

Pros

- You can repay your total outstanding balance at once

- You replace your high interest debts with a comparatively low interest loan

- You have to make only a single monthly payment

Cons

- May lose collateral if you cannot repay the loan on time

When to opt for

- You have collateral to pledge in order to obtain a loan

- You are confident to make the monthly payments to repay the new loan on time

- Want to lower your interest rates

- Want to repay bills through low monthly payment

Balance Transfer

When you opt for balance transfer method, with your creditors’ approval, you actually transfer your high interest bills to a relatively low interest card with sufficient credit limit. Thus, you repay your outstanding dues at a reduced rate of interest.

What to expect:

Pros

- Replace multiple credit cards with a single one

- Pay off outstanding credit card dues at relatively low interest rate

- Can save the money which you’d have to pay if you opt for professional help

Cons

- May fall into debt again if you start using high interest credit cards and not repay dues in every billing cycle

When to opt for

- You’re struggling to manage your high interest credit card bills

- Facing difficulty in remembering due dates of multiple credit cards

- You want to repay debt without any professional help

Bankruptcy

In this debt relief option, you repay your debts through a court monitored repayment plan. You can pay back your creditors through either Chapter 7 or Chapter 13 bankruptcy, depending upon which one you qualify for.

What to expect:

Pros

- Creditors and collection agencies will not contact you for payments

- In Chapter 7 bankruptcy, you can become debt free within 3-4 months

- It will put stay on impending lawsuits

- Your creditors will not be able to garnish your wage

Cons

- Your credit score will get reduced by about 200 points depending upon your present score

When to opt for

- You want to make a fresh financial start

- This is your last option to get rid of your financial obligations

Self Repayment Plan

This is where you repay your debts on your own following the basic financial principles such as budgeting, saving along with reducing irrelevant expenditures.

What to expect:

Pros

- Don’t have to pay professional fees

- Can avoid being scammed by imposters posing as professionals

- Positive impact on credit report after paying off debt

Cons

- Cannot be successful if cannot plan a budget or if you spend extravagantly

When to opt for

- You’re good at planning a realistic budget and following it

- You are confident to repay debts on your own

- You are late on your monthly payments

- You can convince your creditors for an alternative payment plan

Debt Relief Options - Types of bills you can repay

Unsecured bills such as:

- Debts incurred through medical treatment

- Bills acquired through cash advance loans

- Debts assigned to collection agencies

- Bills accumulated through credit card purchases

- Debts accrued through utility services

Debt Relief Companies - How to find a reliable one

Check out company accreditations

Go through the client testimonials

Check out the service background

Compare the fee structure

Debt Relief Act - 6 Facts you must know

Before you decide to work with a debt relief company for credit card debt relief and other bill repayment strategies, check out the rules and regulations in the Debt Relief Act. Being aware will help you avoid getting scammed.

- The companies can’t ask consumers to pay an upfront fee verbally or in writing

- The companies can’t make false promises to the consumers

- The companies have to inform consumers about the tenure and different aspects of the programs

- The companies can charge fees after negotiating/reducing/settling debt

- The consumers need to pay fee and save money in a dedicated account

- The consumers will have full access to the account

3 Popular debt relief options - Outlining the effects to your credit

I want to lay out some facts Read more...

There is much more to discuss on this topic, but for the consumer struggling with debt my point is, stop thinking about your score. Additional credit availability is unlikely right now, anyway.

The credit score has been so indoctrinated into our consumer based society that people make irrational decisions, negatively impacting themselves and their families, all in the name of the all mighty FICO.

So, I would say "Put down that credit report and step away from the ledge"!

If you're struggling with debt, whatever the hardship, and are forced to consider your options, I will lay out the legitimate options and outline the effects to your credit.The 3 options (DMP, Debt Settlement, and Bankruptcy) are what a consumer, who cannot keep up with payments, has to consider. The fact is, every one of them is going to hurt your ability to obtain new credit products. Even just slogging along and struggling to meet your minimums is going to keep you from any new credit based on a poor DTI ratio, regardless of the FICO score.

Basing your decision on which option to go with because of the effect on your credit report, is like arguing over whether to punch a one foot or two foot hole in the bottom of the boat while at sea. The boat sinks no matter what.

Chapter 7 bankruptcy and shorter duration debt settlement strategies actually track pretty well with each other when you boil them down to which one will put you in position to obtain legitimate loans, like a home/car purchase or student loans, the quickest.

Credit counseling programs may not provide the earliest opportunities to obtain new credit card accounts, but this option can track well with settling accounts and access to fairly priced home, auto and student loans.

The point of this article is, when you are drowning in debt and worried about your credit score, you're worried about the wrong thing!

The media, lenders, regulators, unwitting commentators, have all contributed to the credit score hype. Sure, it is important when you are out shopping for loans and better interest rates, but that's not what someone who cannot keep their payments up should be thinking about. They are not going to get credit, and they cannot service the additional debt anyway. Anyone saying something different is talking up their book, has the luxury of not struggling with debt, or is motivated by some special interest.

When determining which debt relief option will best suit your situation, and your mid-to-long term goals, always start with the math. The math doesn't lie and should assist you in narrowing down which option is best.

Chapter 7, for those who qualify, and who fully understand all of the implications associated with filing (sans the credit score), will provide the quickest, most thorough relief.

Other than a discharge through bankruptcy, my experience would suggest that consumers weigh and compare credit counseling and a debt management plan (DMP) beside a debt settlement approach, and make a rational decision based on the math and the flexibility that is built into either option.

Settlement will win the flexibility test. When doing the math to qualify for a DMP, and when considering the current average, you will need to factor your ability to consistently and comfortably make a monthly payment of 2.1% of your current unsecured credit card balances. If you cannot, or question your ability to maintain this type of lower monthly payment, I question why you would even start a DMP. You have a high probability of not completing it and will have wasted resources that would have contributed to your success using a settlement approach and the ability to regain your financial freedom sooner.

Get your unmanageable debt dealt with and your life back first. Credit can be repaired and your score will recover.

Industry Expert